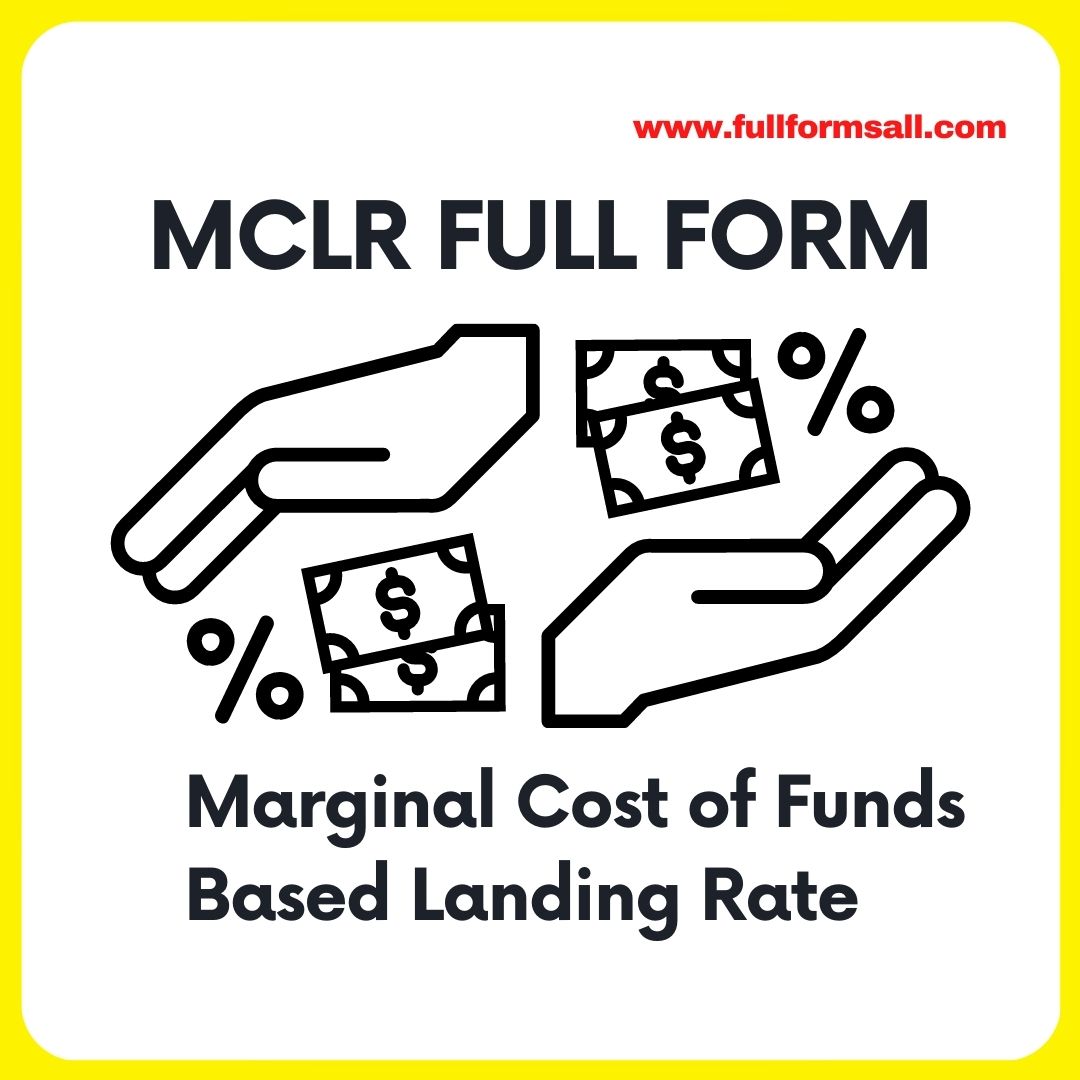

In this article you get to know about MCLR full from and other different abbreviations of MCLR in various fields. MCLR full form refers to Marginal Cost of Funds Based Landing Rate.

Marginal Cost of Funds Based Lending Rate is a lending rate that is calculated by banks based on the marginal cost of funds. MCLR is the minimum interest rate at which a bank can lend, and it is determined by the cost of funds of a bank. MCLR was introduced by the Reserve Bank of India in April 2016, and it replaced the base rate system.

MCLR is calculated based on four components:

| Marginal cost of funds |

| Negative carry on account of cash reserve ratio |

| Operating cost |

| Tenor premium |

Marginal cost of funds: This refers to the cost of borrowing or acquiring funds for the bank. It includes the cost of deposits, borrowings, and other liabilities. The marginal cost of funds is calculated by considering the latest interest rates paid by the bank on different types of deposits, such as savings accounts, fixed deposits, and current accounts.

Negative carry on account of cash reserve ratio: All banks in India are required to maintain a certain percentage of their deposits with the RBI as a cash reserve ratio. This means that banks cannot use this portion of their funds to lend or invest. Therefore, the cost of maintaining this reserve has to be factored into the MCLR calculation.

Operating cost: This component includes the expenses incurred by the bank in carrying out its day-to-day operations, such as salaries, rent, electricity, etc.

Tenor premium: This refers to the additional interest rate charged by the bank for the period of the loan. It takes into account the time value of money and the risk associated with lending for a longer period.

The formula for calculating MCLR is as follows:

MCLR = Marginal cost of funds + Negative carry on account of CRR + Operating cost + Tenor premium

For example, let’s say that a bank has a marginal cost of funds of 8%, a negative carry of 0.5% due to CRR, operating cost of 1%, and a tenor premium of 0.25%. The MCLR of this bank would be:

MCLR = 8% + 0.5% + 1% + 0.25% = 9.75%

This means that the minimum interest rate at which this bank can lend money would be 9.75%.

It’s important to note that MCLR is reviewed and revised by banks every month, depending on the changes in the cost of funds and other components. The MCLR rate applicable to a borrower is based on the tenor of the loan, and it is usually reset on a yearly basis. If the MCLR rate increases, the interest rate on the loan also increases, and vice versa.

When MCLR increases, it directly affects the interest rate of loans for borrowers. The impact of an MCLR increase depends on the type of loan. Here are some of the potential consequences:

Home loans: If MCLR increases, the interest rate on home loans will also increase. This means that borrowers will have to pay more in monthly installments, which could strain their finances. It may also make it more difficult for borrowers to qualify for a loan, as the higher interest rate could increase their debt-to-income ratio.

Personal loans: Similar to home loans, an increase in MCLR will lead to an increase in interest rates for personal loans. This means that borrowers will have to pay more in interest charges and higher monthly installments. This could make personal loans less affordable for some borrowers, who may look for alternative financing options.

Business loans: An increase in MCLR could affect businesses that rely on loans for operations or expansion. Higher interest rates could increase the cost of capital for businesses, making it more difficult to borrow funds. This could lead to decreased investment and growth opportunities.

Fixed deposit rates: When MCLR increases, it often leads to an increase in fixed deposit rates as well. This means that savers can earn more interest on their deposits, which can be a positive for those relying on interest income. However, it could also reduce the attractiveness of loans as borrowers may prefer to invest in fixed deposits instead.

An increase in MCLR could lead to higher borrowing costs for individuals and businesses. This could lead to reduced demand for loans, slower economic growth, and financial strain for borrowers.

The Marginal Cost of Funds Based Lending Rate has had a significant impact on banks. Here are some of the effects of MCLR on banks:

Improved transmission of policy rates: MCLR has made the transmission of policy rates more efficient. Banks are now required to review and revise their MCLR rates on a monthly basis, which ensures that the changes in policy rates are quickly passed on to borrowers.

Increased transparency: MCLR has made the lending rate system more transparent. Borrowers now have a better understanding of how their loan interest rates are calculated, and banks are required to publish their MCLR rates on their websites.

Higher volatility in lending rates: With the introduction of MCLR, lending rates have become more volatile. This is because MCLR rates are revised on a monthly basis, which means that borrowers could experience fluctuations in their loan interest rates.

Better asset-liability management: Banks need to manage their assets and liabilities effectively to maintain their profitability. MCLR has forced banks to be more diligent in their asset-liability management as they need to factor in their cost of funds, negative carry on account of cash reserve ratio, operating cost, and tenor premium to calculate their MCLR.

Increased competition: MCLR has led to increased competition among banks. Banks need to offer competitive MCLR rates to attract borrowers, which has led to a reduction in lending rates in some cases.

Impact on profitability: MCLR has had a mixed impact on bank profitability. On the one hand, it has led to increased competition and improved asset-liability management. On the other hand, the volatility in lending rates could impact the profitability of banks.

Marginal Cost of Funds Based Lending Rate has had a significant impact on banks. It has led to increased transparency, improved transmission of policy rates, and increased competition. However, it has also led to higher volatility in lending rates and could impact the profitability of banks.

Different abbreviations of MCLR in various fields are as follows

| Term | Abbreviation | Category |

| MCLR | Microcystin-LR | Medical |

| MCLR | Maximum Cell Loss Ratio | Technology |

| MCLR | McLaughlin Line Railroad | Travel |

| MCLR | Marginal Cost of funds based Lending Rate | Business |

| MCLR | Midwest Consortium for Latino Research | Others |

| MCLR | Midwest Center for Labor Research | Others |

| MCLR | Medium Capacity Long Range | Others |

CONCLUSION:

Dear reader in this article you get to know about MCLR full from and MCLR term used in various other fields, If you have any query regarding this article kindly comment below.